On the day that the Dutch government announced EUR 450 million co-funding for the development of a Gasunie (Dutch Gas TSO) 6.000 tonnes hydrogen storage facility, and the EU Commission endorsed a French aid program aimed at 1 GW of renewable and low-carbon hydrogen production totalling EUR797 million, the Clean Hydrogen Partnership, CHP on July 7, 2026 published its State of the Clean Hydrogen Valleys Sector Report, Developing Hydrogen Valleys in a Challenging Market Environment (H2V Sector Report).

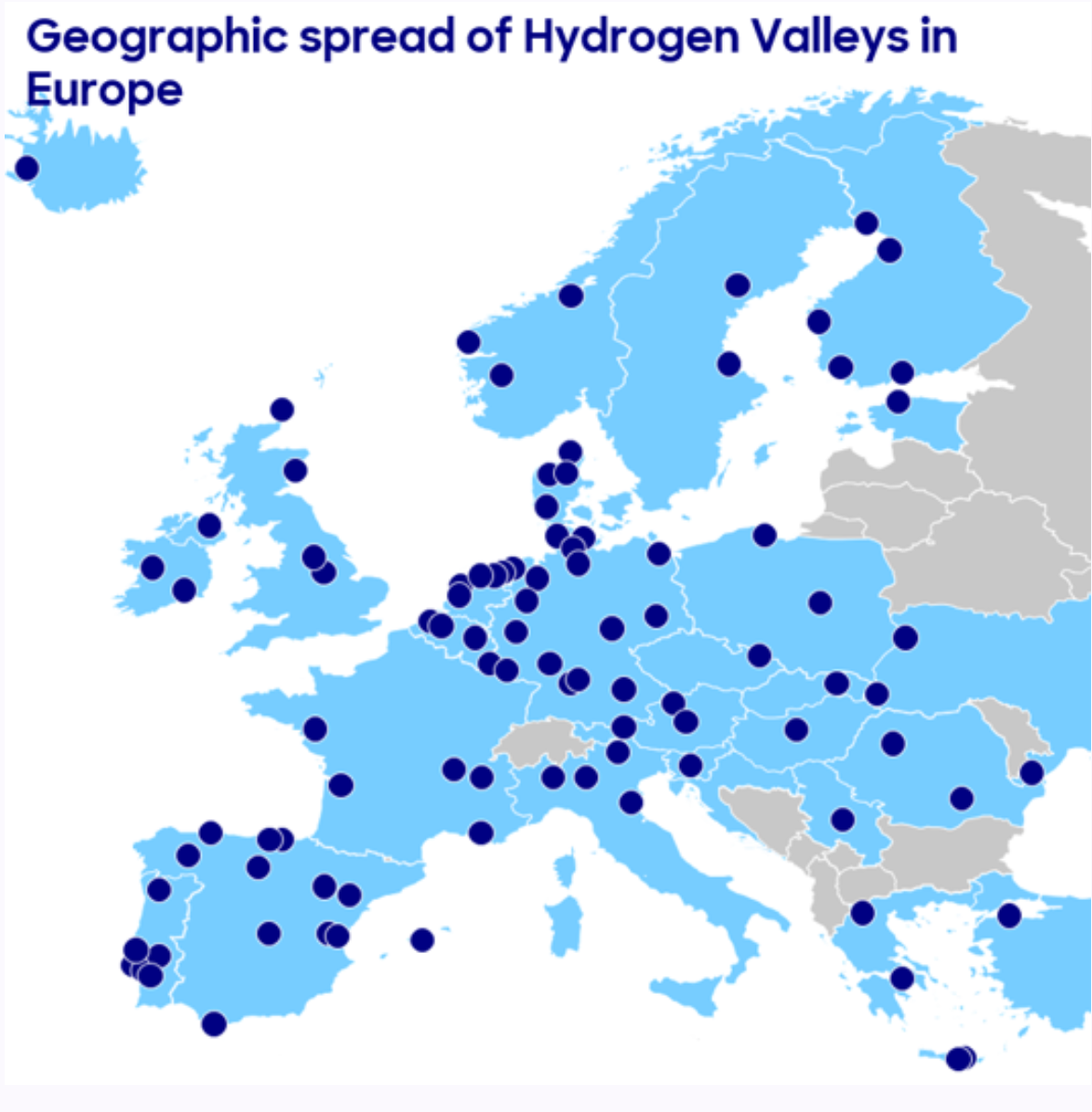

The H2V Sector Report delivers statistical insights into Hydrogen Valley project fundamentals, a current market sentiment survey among Hydrogen Valley representatives, and targeted recommendations for policymakers, investors, and project developers. The findings draw on data from 106 Hydrogen Valley projects worldwide – of which 91% are located in Europe, 5% in the Americas, 2% in the Middle East, and 2% in Asia-Pacific – and are based on a completely redesigned data survey as of April 2026. Accounting for the large majority of the over 600 MW of operational electrolyser capacity in Europe today, and representing a significant share of the more than 3.3 GW that has passed Final Investment Decision, Hydrogen Valleys have demonstrated that they are the building blocks from which a European clean hydrogen sector will be constructed, one regional ecosystem at a time. The Clean Hydrogen Partnership has supported 27 valleys, so far, representing EUR 1.6 billion total public funding of EURO 328 million – a leverage factor of almost 5 times.

Global project pipeline includes 440 GW of announced electrolyser capacity by 2030, Hydrogen Valleys are the key drivers behind this growth and the backbone of the sector scale-up. H2V Platform projects:

- …. totalled 7.8 GW electrolzyer capacity in the pipeline in Europe alone, of which 1.3 GW post-FID.

- …. represent EUR 134 bn (EUR 47 bn in Europe) in planned CAPEX investment and a total planned electrolyser capacity of approximately 21 GW.

With mobility as the main end-use in Hydrogen Valleys, it is striking that the coordination of hydrogen valley development along EU’s main corridors is still in its infancy, as well as proactive linking to large production and storage locations as mentioned above.

Hopefully the recently approved Tripartite agreement of 22 Member States on accelerating energy storage facilities, to between 30-35 GW of storage capacity in Europe, could facilitate concrete actions on the corridors in the next two years.

As part of the agreement, developers of energy storage and renewable energy projects will provide yearly estimates of new energy storage and hybrid projects and their volumes, while energy-consuming industries have committed to developing energy storage projects at their own sites and to giving clearer information about when and how much electricity they use. This visibility on the projects pipeline is essential to provide clarity and certainty to investors.

On their side, Member States will support the energy storage sector by removing barriers that slow progress. They committed to enable the National Regulatory Authorities to set or approve cost-reflective and non-discriminatory network tariffs that stimulate flexibility. Where necessary, Member States will provide financial support for energy storage rollout and manufacturing through national and EU funding, and in line with State aid rules, such as the Clean Industrial State Aid Framework (CISAF).